You’re asking the big question…

Is Nvidia stock too expensive?

Looking at the share price in isolation won’t tell you much. You have to compare that price tag to the actual cash the company is generating.

Based on the data from January 2026, here is a clearer look at the numbers and future expectations.

The Valuation Metrics

To judge if the stock is overvalued, you need to compare what you are paying to what the company is earning.

P/E Ratio (Price-to-Earnings)

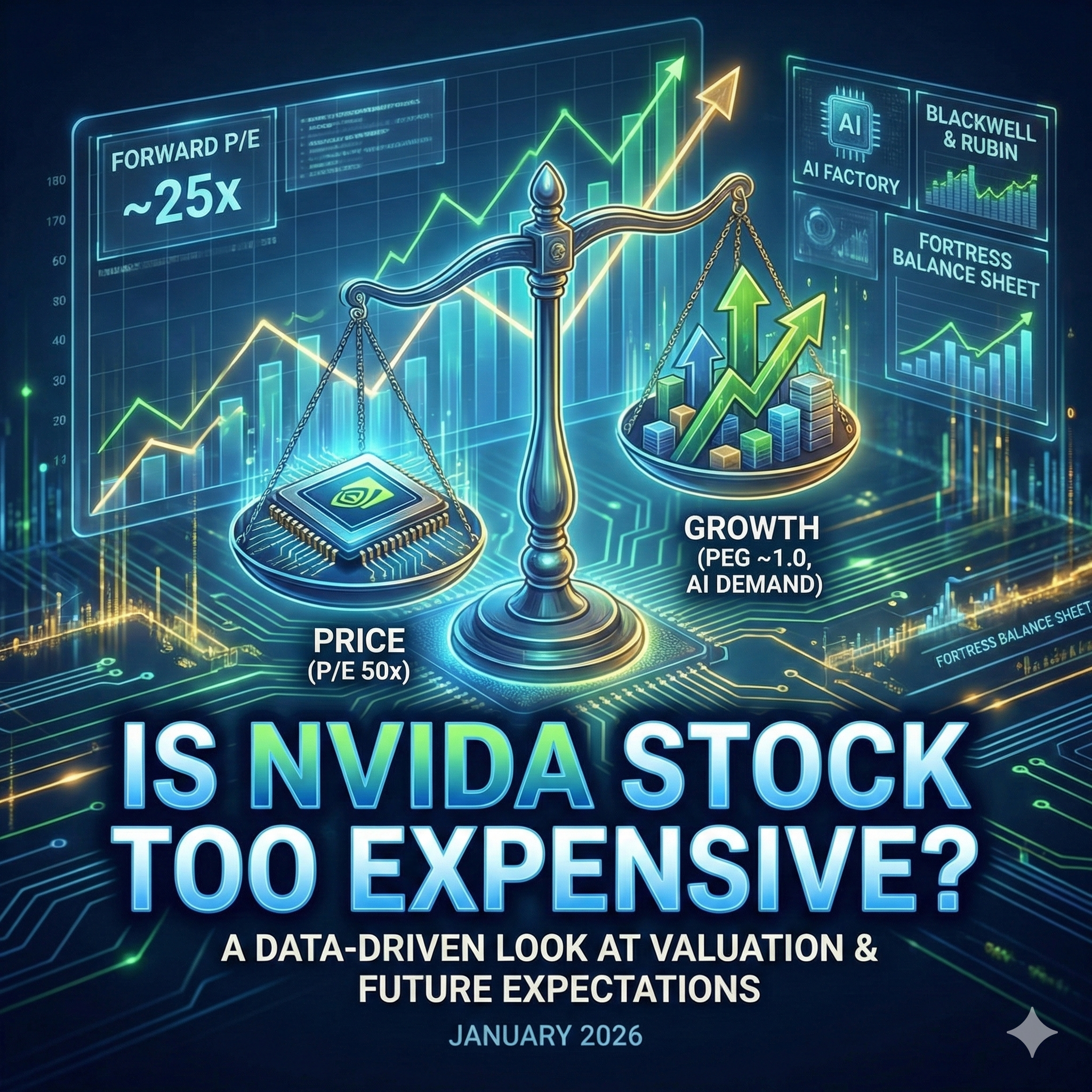

- Current Situation: you are currently paying about 46x to 52x earnings for the stock.

- The Reality: historically, this is high relative to the S&P 500 average, which usually sits around 20x. However, for a technology company growing at this speed, the market often assigns a growth premium. essentially, you are paying for the expectation of future dominance.

Forward P/E (Future Earnings)

This metric is arguably more important for you to consider. It compares the price you pay today to what Nvidia is expected to earn over the next 12 months.

- What it means: the forward P/E drops significantly – projected to move toward ~25x–30x by 2027. The stock appears expensive based on last year’s earnings, but looks much more reasonable when weighed against next year’s projections.

PEG Ratio (Price/Earnings-to-Growth)

This is a critical check for growth stocks. It asks: Is the high price justified by the growth rate?

- The Rule: a PEG of 1.0 is generally considered fair value.

- The Reality: Nvidia is hovering right around 1.0. This implies the stock is fairly valued. Even though the P/E multiple is high, the earnings growth (often doubling year-over-year) supports the valuation.

Price-to-Sales (The Risk Metric)

Nvidia trades at a very high multiple of its total sales (often >20x).

- The Risk: this is the strongest argument for the stock being overvalued. It means you are paying a huge premium for every dollar of revenue, which assumes Nvidia will maintain its exceptionally high profit margins (70%+) indefinitely.

Future Expectations: The Bull Case

The current valuation is pinned to three main pillars. If these persist, the stock may justify its price.

AI Demand is Broadening

Demand has moved beyond simple chatbots. We are now seeing Sovereign AI (nations building their own infrastructure) and industrial robotics.

CEO Jensen Huang points to a $500B+ opportunity in data center infrastructure alone. As long as major tech companies (Microsoft, Meta, Google) continue their capital spending, Nvidia’s revenue baseline remains secure.

The AI Factory Transition

Data centers are evolving into AI Factories.

Nvidia isn’t just selling chips.

They are selling the entire architecture – cables, switches, and software. The backlog for their cloud GPUs extends well into 2026. When demand outstrips supply for this long, it typically suggests earnings have not yet peaked.

Technological Lead (Blackwell & Rubin)

Nvidia’s primary advantage is the speed of its innovation.

- Blackwell: these chips are ramping up now, offering significant efficiency gains.

- Rubin: the next-generation architecture (slated for 2026/2027) forces competitors like AMD to chase a moving target.

- Impact: as long as Nvidia maintains a 1-2 year lead, they can maintain pricing power, protecting the margins that support the stock price.

Why a High P/E Isn’t Always Bad

Scenario A: The Strong Balance Sheet

A high P/E (e.g., 50x) is risky if a company is carrying heavy debt. Nvidia, however, has a fortress balance sheet – zero net debt and massive free cash flow.

- Why it matters: they can self-fund innovation without borrowing. It also provides a safety net. If the stock price dips, the company has the cash to buy back its own shares, which supports the price.

Scenario B: Valuation Compression

Investors often worry that for a P/E ratio to drop, the stock price must crash. That is incorrect. The P/E ratio can flatten or drop even if the stock price stays the same or rises. This is called PE Compression.

P/E = Price/Earnings

Imagine a stock you own trades at $100 and earns $2 per share.

- P/E = 50x (Expensive)

Now, imagine the company doubles its earnings to $4 per share, but the stock price stays at $100.

- P/E = 25x (Cheap)

The result: the stock price didn’t crash, but the valuation was cut in half – is it more or less valuable?!

This is exactly what has happened to Nvidia repeatedly. The stock price rises, but earnings rise faster, causing the P/E multiple to compress.

This is why looking at Forward P/E is often more useful than current P/E for high-growth companies.

The Final Word

So, where does this leave you? Nvidia is not a bargain-bin stock. You are paying a premium price. But you are buying a premium company. If you believe the AI revolution is just getting started, the valuation is justifiable. If you think AI is a bubble about to pop, it is drastically overvalued. The math supports the bull case, but your stomach needs to handle the volatility.

Frequently Asked Questions (FAQ)

Is it too late for me to buy?

- The short answer: not necessarily.

- The context: if you are trading for next week, it’s a toss-up. If you are investing for 2030, and you believe in the $500B data center expansion, the company still has room to grow into its valuation.

What is the biggest risk I should watch for?

- The danger: customer concentration. A huge chunk of revenue comes from just a few companies like Microsoft and Meta. If they decide to cut spending or build their own chips successfully, Nvidia’s earnings could take a hit.

Why does the stock sometimes drop even when earnings are good?

- The reason: expectations are sky-high. When a stock is “priced for perfection,” simply being “good” isn’t enough. Wall Street sometimes wants a massive beat, and if they don’t get it, they sell.

How does this compare to the Dot-Com bubble?

- The difference: in 2000, companies had high stock prices but no profits. Nvidia has massive profits and real cash flow today. It is a real business, not just a hype machine.